![]()

-

뉴스

-

- Hactl Launches Autonomous Ramp Vehicle Operations

- Hong Kong Air Cargo Terminals Limited (Hactl) – Hong Kong’s largest independent cargo handler – is progressing its plan to introduce Autonomous Electric Tractors (AETs) to its ramp operations in 2024. Hactl has signed a Memorandum of Understanding (MOU) w...

-

- Maersk’s New Warehouse in Sri Lanka to Strengthen...

- The new 100,000 sq. ft. facility, with export consolidation and 3PL services, lies close to key manufacturing hubs, consumption markets, and port infrastructure for quick turnaround times. A.P. Moller – Maersk (Maersk) today inaugurated its brand new warehouse in...

-

- ONE Hosted 3rd Container Shipping Summit in Nagasak...

- Ocean Network Express (ONE) proudly hosted the 3rd Container Shipping Summit at Dejima, Nagasaki on 26 March 2024, in collaboration with Anchor Ship Partners Co.,Ltd., The Juhachi-Shinwa Bank,Ltd., and KOZO KEIKAKU ENGINEERING INC. It has been a year since the first su...

-

- Qatarenergy Enters Time Charter Agreements with Nak...

- QatarEnergy signed time-charter party (TCP) agreements with Qatar Gas Transport Company Limited (Nakilat) for the operation of 25 conventional-size LNG vessels as part of the second ship-owner tender under QatarEnergy’s historic LNG Fleet Expansion Program. The agree...

-

- 운항스케줄

-

오피니언

2021-09-13 09:06

논단/ 2015년 영국보험법과 해상보험에서의 고지의무와 워런티 법리의 변화

정해덕 법무법인 화우 변호사(법학박사)

2015년 영국보험법의 제정, 시행에 따라 영국해상보험법상의 고지의무와 워런티에 관한 법리도 수정, 변경되었으므로 이에 대한 검토, 연구가 요망됨

다. 2015년 영국보험법 관련 규정

2015년 영국보험법 제8조와 부록 1의 규정을 살펴보면 다음과 같다.

8 Remedies for breach

(1)The insurer has a remedy against the insured for a breach of the duty of fair presentation only if the insurer shows that, but for the breach, the insurer (a)would not have entered into the contract of insurance at all, or (b)would have done so only on different terms.

(2)The remedies are set out in Schedule 1.

(3)A breach for which the insurer has a remedy against the insured is referred to in this Act as a “qualifying breach”.

(4)A qualifying breach is either (a)deliberate or reckless, or (b)neither deliberate nor reckless.

(5)A qualifying breach is deliberate or reckless if the insured (a)knew that it was in breach of the duty of fair presentation, or (b)did not care whether or not it was in breach of that duty.

(6)It is for the insurer to show that a qualifying breach was deliberate or reckless.

SCHEDULE 1

Insurers’ remedies for qualifying breaches

This schedule has no associated Explanatory Notes

PART 1 Contracts

General

1 This Part of this Schedule applies to qualifying breaches of the duty of fair presentation in relation to non-consumer insurance contracts

Deliberate or reckless breaches

2 If a qualifying breach was deliberate or reckless, the insurer (a)may avoid the contract and refuse all claims, and (b)need not return any of the premiums paid.

Other breaches

3 Paragraphs 4 to 6 apply if a qualifying breach was neither deliberate nor reckless.

4 If, in the absence of the qualifying breach, the insurer would not have entered into the contract on any terms, the insurer may avoid the contract and refuse all claims, but must in that event return the premiums paid.

5 If the insurer would have entered into the contract, but on different terms (other than terms relating to the premium), the contract is to be treated as if it had been entered into on those different terms if the insurer so requires.

6 (1)In addition, if the insurer would have entered into the contract (whether the terms relating to matters other than the premium would have been the same or different), but would have charged a higher premium, the insurer may reduce proportionately the amount to be paid on a claim.

(2)In sub-paragraph (1), “reduce proportionately” means that the insurer need pay on the claim only X% of what it would otherwise have been under an obligation to pay under the terms of the contract (or, if applicable, under the different terms provided for by virtue of paragraph 5), where

PART 2 Variations

General

7 This Part of this Schedule applies to qualifying breaches of the duty of fair presentation in relation to variations to non-consumer insurance contracts.

Deliberate or reckless breaches

8 If a qualifying breach was deliberate or reckless, the insurer

(a)may by notice to the insured treat the contract as having been terminated with effect from the time when the variation was made, and

(b)need not return any of the premiums paid.

Other breaches

9 (1)This paragraph applies if (a)a qualifying breach was neither deliberate nor reckless, and (b)the total premium was increased or not changed as a result of the variation.

(2)If, in the absence of the qualifying breach, the insurer would not have agreed to the variation on any terms, the insurer may treat the contract as if the variation was never made, but must in that event return any extra premium paid.

(3)If sub-paragraph (2) does not apply (a)if the insurer would have agreed to the variation on different terms (other than terms relating to the premium), the variation is to be treated as if it had been entered into on those different terms if the insurer so requires, and (b)paragraph 11 also applies if (in the case of an increased premium) the insurer would have increased the premium by more than it did, or (in the case of an unchanged premium) the insurer would have increased the premium.

10 (1)This paragraph applies if (a)a qualifying breach was neither deliberate nor reckless, and (b)the total premium was reduced as a result of the variation.

(2)If, in the absence of the qualifying breach, the insurer would not have agreed to the variation on any terms, the insurer may treat the contract as if the variation was never made, and paragraph 11 also applies.

(3)If sub-paragraph (2) does not apply (a)if the insurer would have agreed to the variation on different terms (other than terms relating to the premium), the variation is to be treated as if it had been entered into on those different terms if the insurer so requires, and (b)paragraph 11 also applies if the insurer would have increased the premium, would not have reduced the premium, or would have reduced it by less than it did.

Proportionate reduction

11 (1)If this paragraph applies, the insurer may reduce proportionately the amount to be paid on a claim arising out of events after the variation.

(2)In sub-paragraph (1), “reduce proportionately” means that the insurer need pay on the claim only Y% of what it would otherwise have been under an obligation to pay under the terms of the contract (whether on the original terms, or as varied, or under the different terms provided for by virtue of paragraph 9(3)(a) or 10(3)(a), as the case may be), where

(3)In the formula in sub-paragraph (2), “P” (a)in a paragraph 9(3)(b) case, is the total premium the insurer would have charged, (b)in a paragraph 10(2) case, is the original premium, (c)in a paragraph 10(3)(b) case, is the original premium if the insurer would not have changed it, and otherwise the increased or (as the case may be) reduced total premium the insurer would have charged.

PART 3 Supplementary

Relationship with section 84 of the Marine Insurance Act 1906

12 Section 84 of the Marine Insurance Act 1906 (return of premium for failure of consideration) is to be read subject to the provisions of this Schedule in relation to contracts of marine insurance which are non-consumer insurance contracts.

<계속>

다. 2015년 영국보험법 관련 규정

2015년 영국보험법 제8조와 부록 1의 규정을 살펴보면 다음과 같다.

8 Remedies for breach

(1)The insurer has a remedy against the insured for a breach of the duty of fair presentation only if the insurer shows that, but for the breach, the insurer (a)would not have entered into the contract of insurance at all, or (b)would have done so only on different terms.

(2)The remedies are set out in Schedule 1.

(3)A breach for which the insurer has a remedy against the insured is referred to in this Act as a “qualifying breach”.

(4)A qualifying breach is either (a)deliberate or reckless, or (b)neither deliberate nor reckless.

(5)A qualifying breach is deliberate or reckless if the insured (a)knew that it was in breach of the duty of fair presentation, or (b)did not care whether or not it was in breach of that duty.

(6)It is for the insurer to show that a qualifying breach was deliberate or reckless.

SCHEDULE 1

Insurers’ remedies for qualifying breaches

This schedule has no associated Explanatory Notes

PART 1 Contracts

General

1 This Part of this Schedule applies to qualifying breaches of the duty of fair presentation in relation to non-consumer insurance contracts

Deliberate or reckless breaches

2 If a qualifying breach was deliberate or reckless, the insurer (a)may avoid the contract and refuse all claims, and (b)need not return any of the premiums paid.

Other breaches

3 Paragraphs 4 to 6 apply if a qualifying breach was neither deliberate nor reckless.

4 If, in the absence of the qualifying breach, the insurer would not have entered into the contract on any terms, the insurer may avoid the contract and refuse all claims, but must in that event return the premiums paid.

5 If the insurer would have entered into the contract, but on different terms (other than terms relating to the premium), the contract is to be treated as if it had been entered into on those different terms if the insurer so requires.

6 (1)In addition, if the insurer would have entered into the contract (whether the terms relating to matters other than the premium would have been the same or different), but would have charged a higher premium, the insurer may reduce proportionately the amount to be paid on a claim.

(2)In sub-paragraph (1), “reduce proportionately” means that the insurer need pay on the claim only X% of what it would otherwise have been under an obligation to pay under the terms of the contract (or, if applicable, under the different terms provided for by virtue of paragraph 5), where

PART 2 Variations

General

7 This Part of this Schedule applies to qualifying breaches of the duty of fair presentation in relation to variations to non-consumer insurance contracts.

Deliberate or reckless breaches

8 If a qualifying breach was deliberate or reckless, the insurer

(a)may by notice to the insured treat the contract as having been terminated with effect from the time when the variation was made, and

(b)need not return any of the premiums paid.

Other breaches

9 (1)This paragraph applies if (a)a qualifying breach was neither deliberate nor reckless, and (b)the total premium was increased or not changed as a result of the variation.

(2)If, in the absence of the qualifying breach, the insurer would not have agreed to the variation on any terms, the insurer may treat the contract as if the variation was never made, but must in that event return any extra premium paid.

(3)If sub-paragraph (2) does not apply (a)if the insurer would have agreed to the variation on different terms (other than terms relating to the premium), the variation is to be treated as if it had been entered into on those different terms if the insurer so requires, and (b)paragraph 11 also applies if (in the case of an increased premium) the insurer would have increased the premium by more than it did, or (in the case of an unchanged premium) the insurer would have increased the premium.

10 (1)This paragraph applies if (a)a qualifying breach was neither deliberate nor reckless, and (b)the total premium was reduced as a result of the variation.

(2)If, in the absence of the qualifying breach, the insurer would not have agreed to the variation on any terms, the insurer may treat the contract as if the variation was never made, and paragraph 11 also applies.

(3)If sub-paragraph (2) does not apply (a)if the insurer would have agreed to the variation on different terms (other than terms relating to the premium), the variation is to be treated as if it had been entered into on those different terms if the insurer so requires, and (b)paragraph 11 also applies if the insurer would have increased the premium, would not have reduced the premium, or would have reduced it by less than it did.

Proportionate reduction

11 (1)If this paragraph applies, the insurer may reduce proportionately the amount to be paid on a claim arising out of events after the variation.

(2)In sub-paragraph (1), “reduce proportionately” means that the insurer need pay on the claim only Y% of what it would otherwise have been under an obligation to pay under the terms of the contract (whether on the original terms, or as varied, or under the different terms provided for by virtue of paragraph 9(3)(a) or 10(3)(a), as the case may be), where

(3)In the formula in sub-paragraph (2), “P” (a)in a paragraph 9(3)(b) case, is the total premium the insurer would have charged, (b)in a paragraph 10(2) case, is the original premium, (c)in a paragraph 10(3)(b) case, is the original premium if the insurer would not have changed it, and otherwise the increased or (as the case may be) reduced total premium the insurer would have charged.

PART 3 Supplementary

Relationship with section 84 of the Marine Insurance Act 1906

12 Section 84 of the Marine Insurance Act 1906 (return of premium for failure of consideration) is to be read subject to the provisions of this Schedule in relation to contracts of marine insurance which are non-consumer insurance contracts.

<계속>

< 코리아쉬핑가제트 >

선박운항스케줄

인기 스케줄

-

BUSAN

GDANSK

GDANSK선박운항스케줄 목록 - 선박운항스케줄목록으로 Vessel, D-Date, A-Date, Agent를 나타내는 테이블입니다. Vessel D-Date A-Date Agent Cma Cgm Kimberley 04/19 06/07 CMA CGM Korea Cma Cgm Tenere 04/19 06/07 CMA CGM Korea Ever Burly 04/25 06/11 Evergreen -

BUSAN

BANDAR ABBAS선박운항스케줄 목록 - 선박운항스케줄목록으로 Vessel, D-Date, A-Date, Agent를 나타내는 테이블입니다. Vessel D-Date A-Date Agent Ren Jian 23 04/19 06/02 KWANHAE SHIPPING TBN-WOSCO 04/19 06/03 Chun Jee Esl Busan 04/20 05/19 HS SHIPPING -

BUSAN

YANGON선박운항스케줄 목록 - 선박운항스케줄목록으로 Vessel, D-Date, A-Date, Agent를 나타내는 테이블입니다. Vessel D-Date A-Date Agent Wan Hai 335 04/17 05/03 Wan hai Wan Hai 335 04/17 05/10 Interasia Lines Korea Wan Hai 503 04/17 05/10 Interasia Lines Korea -

INCHEON

QINHUANGDAO선박운항스케줄 목록 - 선박운항스케줄목록으로 Vessel, D-Date, A-Date, Agent를 나타내는 테이블입니다. Vessel D-Date A-Date Agent Xin Yu Jin Xiang 04/19 04/20 Qin-IN Ferry Xin Yu Jin Xiang 04/22 04/23 Qin-IN Ferry Xin Yu Jin Xiang 04/26 04/27 Qin-IN Ferry -

BUSAN

SAVANNAH선박운항스케줄 목록 - 선박운항스케줄목록으로 Vessel, D-Date, A-Date, Agent를 나타내는 테이블입니다. Vessel D-Date A-Date Agent Als Luna 04/18 05/15 CMA CGM Korea Toconao 04/19 05/17 MSC Korea Cosco Pride 04/22 05/24 CMA CGM Korea

- 출발항

-

- 도착항

-

많이 본 기사

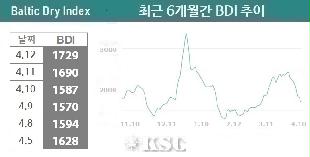

- 톤세제 이후 국적선박 4배 급증…경제효과 입증국제해운대리점協 골프모임 청록회, 400회 맞아 화합 다져‘얼라이언스 재편 대응’ HMM, 2030년까지 150만TEU 선단 확보칼럼/ 한화해운과 한국해운의 미래상BDI 1729포인트…금주 벌크 시황 상승세 기대북미서안항만 물동량 올해 첫 두달간 20% 급증…“철송 지연은 악화”내항선사도 중소선사 특별지원프로그램 혜택받는다왈레니우스윌헬름센, 볼티모어 사고로 최대 140억 손실 예상HMM, 신입사원과 영종도 거잠포해변 정화활동일본 스미토모중기계공업, 상선건조사업 철수

- 한진, 해외직구 급증에 인천공항 통관시설 100억 투자화촉/ 임기택 IMO 명예사무총장 아들항만물류협회, 2024년 항만하역장 근로자 재해예방시설 지원사업 실시물류와환경연구소, ‘로지스올에코텍’으로 사명 변경판례/ 배타적 경제수역 점용료에서 ‘도매가격’이란?인천항 전자상거래 특화구역 민간제안사업 5차 공고 준비롯데택배, 전자상거래 주문·출고 자동화 서비스 ‘원스톱OMS’ 출시2030년까지 국적 컨선대 200만TEU로 증강해양수산연수원, ‘대한민국 창조경영 2024’서 보건부장관상 수상YGPA, 중기부 공공기관 동반성장 평가서 창립최초 ‘최우수’ 달성

스케줄 많이 검색한 항구

해사물류 통계 ![]()

COPYRIGHTⓒ 2014 KOREA SHIPPING GAZETTE. ALL RIGHTS RESERVED.

COPYRIGHTⓒ 2015

KOREA SHIPPING GAZETTE. ALL RIGHTS RESERVED.

0/250

확인